")

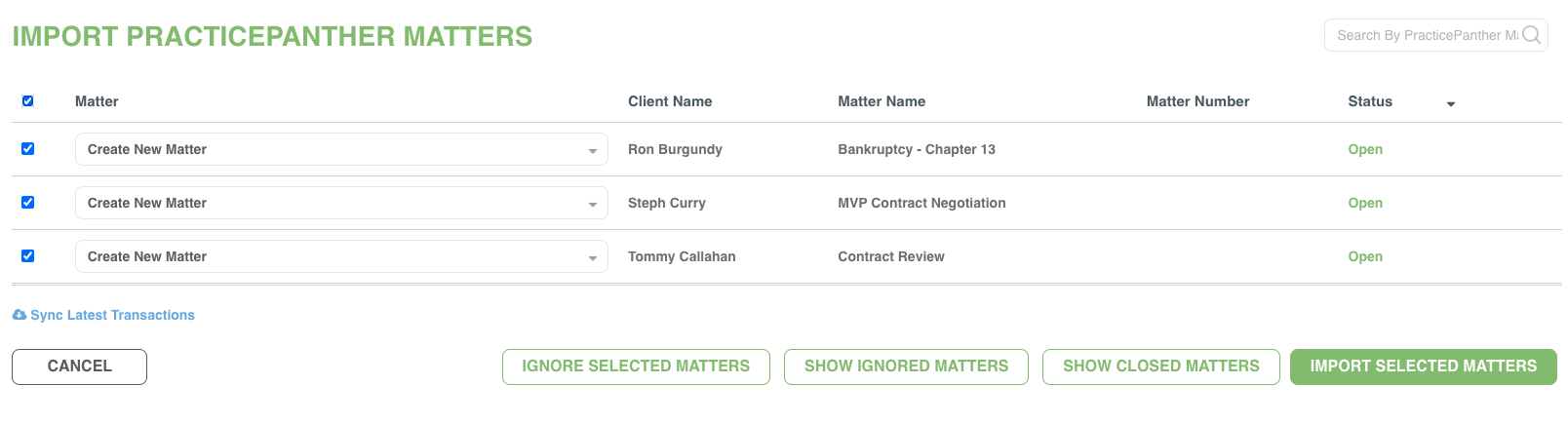

We recently announced that we joined the Paradigm family — a growing legal technology company home to several industry-leading law practice management platforms, including the all-in-one solution, PracticePanther. This was a huge milestone for TrustBooks and in light...